Notes from Taiwan

Electric scooters, nuclear restarts, and offshore wind

The views expressed here are solely my own and do not represent those of my employer

I intended to publish this article a few months ago now, but better late than never.

In early April, I visited Taiwan for just over ten days. I spent the vast majority of my time in Taipei, with a few days in Taichung in the middle of my trip. I thought I’d pull together a random assortment of observations and photos from my trip, covering the energy landscape on the island.

Taiwan had been on my radar for a while, and I’d become much more interested in the country after writing an article comparing Ireland’s offshore wind market to Taiwan’s.

Taipei itself is a bustling city, with the wider metropolitan area having a population of over 7 million people. The metro system is widely regarded as one of the best in the world.

Fuel Prices

One of the first things you notice when you arrive in Taipei is the sheer number of scooters on the streets. Taiwan has one of the highest scooter densities in the world with about 600 scooters per 1,000 people, by far the highest among wealthy nations. There are several reasons for this. Taiwan never built up a big domestic automotive industry in the same way South Korea and Japan did. But probably the primary reason is that it’s just a very affordable way to get around. I was really surprised by how cheap petrol was in Taiwan. Once I converted the prices from New Taiwan dollars (NTD) into euros, I was pretty shocked.

For 95 octane petrol, it was 33.9 NTD per litre, which is the equivalent of about €0.92 per litre. And for context, this photo of the petrol price sign was taken in the midst of the global energy crisis triggered by the U.S.-Iran war. At the time, petrol prices in Ireland were about €1.91 per litre, more than double the price in Taipei.

At first, this really didn’t make sense to me. My mental model for rich East Asian nations like Japan, Korea, and Taiwan was that they would procure energy cargoes, such as oil and LNG, at nearly any price on the international energy market.

So how were retail petrol prices in Taipei during the peak of a global energy crisis this cheap?

Well, the answer is: incredible levels of state intervention and subsidy. It turns out many Asian nations have a very different social contract when it comes to consumer energy prices than we do in much of the West. Even during an energy crisis, the international spot market prices are not passed on to consumers in Taiwan. And this is true not only for liquid fuels like petrol, but also electricity.

This situation stood in stark contrast to what was happening back home in Ireland in April, where the fuel protests brought the country to an effective standstill. Among the wide-ranging demands of the protesters, the two more consistent were the introduction of a fuel price cap and the abolition of the carbon tax.

And as Jack Horgan-Jones said on the Irish Times Inside Politics podcast discussing these two demands:

both of which are red lines the (Irish) government are not willing to cross because they think that the introduction of a fuel cap would be economically ruinous, and leave the exchequer exposed to billions in costs…

And while I agree that the introduction of a fuel price cap would have been a terrible idea, exposing the Exchequer to unacceptably large risks, it was hard to ignore how differently this same issue was treated across two wealthy, hyper-globalised, small island economies, both of which enjoy massive trade surpluses.

When I met an energy industry contact in Taiwan and asked him this very question of how the Taiwanese government could afford this, he simply said, “Well, we have TSMC…” (Taiwan Semiconductor Manufacturing Company).

This comment was clearly somewhat tongue-in-cheek, but there does seem to be a certain truth in it. It made me think about the obvious parallels with the Irish economy and the similar hyper-dependence on a select few corporations for the government’s revenues. But in Ireland, there’s very rarely a clear through line between the huge corporation tax receipts that we receive from tech and pharmaceutical companies, and a tangible benefit that citizens can feel in their pocket. Whereas in Taiwan, this connection is felt directly in the price of petrol at the pump.

And while this is undoubtedly a very inefficient and distortionary use of government revenues, it is hard to deny that it at least gives society a direct sense that they are benefiting from the existence of a certain industry in the country.

Nevertheless, the negative impacts of the fuel price cap in Taiwan are serious. CPC, the state-owned oil company, absorbed NT$17.7 billion (roughly US$550 million) subsidising fuel through the 11-week price freeze during the Iran war. This has put the company under significant financial strain, with massive accumulated losses driven by the government-mandated price-stabilisation measures.

Electric Scooters

Despite these very affordable petrol prices, wandering around the city, I quickly came to realise that a sizeable chunk of the scooters were in fact electric. You could hear them whizzing around with no visible exhaust pipe. Nearly all of these electric scooters were the domestic Taiwanese brand Gogoro. In fact, electric scooters are so commonplace that the Taipei police use them. I stumbled upon several police stations that had a fleet of Gogoro electric scooters parked outside.

Gogoro operates on a battery-swapping model with over 2,500 swapping stations located across Taiwan at nondescript roadside locations. Riders sign up to a subscription service to gain access to the battery-swapping network. Each scooter has two 1.7 kWh battery packs, which riders can quickly remove by flipping up the seat lid. Based on what I observed, the battery swap was very fast, taking less than 30 seconds in many instances before the rider had zoomed off again.

Gogoro also has a partnership with Enel X to use their battery-swapping stations (GoStations) as part of a Virtual Power Plant (VPP). In 2022, Gogoro and Enel X Taiwan’s VPP pilot demonstrated that the Gogoro Network could safely pause charging if there was a grid imbalance or provide energy back to the grid as demand required.

Despite this impressive battery-swapping network, VPP partnership, and seemingly abundant user base across Taiwan, the company is seriously struggling financially. Since listing on the Nasdaq via a SPAC in 2022, their share price has dropped by about 98%. Expanding this very capital-intensive infrastructure into new international markets has proven much harder and slower than investors originally hoped. Nevertheless, other companies are now attempting to launch similar battery-swapping models in Africa and Asia.

Around the time I was in Taiwan, several notable milestones and events occurred.

The AI Chip Boom

The FT reported that Taiwan’s stock market had overtaken the UK’s in total value, driven by record profits from TSMC off the back of booming demand for AI chips. This was a pretty strong reminder that I was somewhere increasingly important to the global economy.

As many people now know, given the increasingly public discussion related to AI, Taiwan and specifically TSMC produce over 90% of the world’s most advanced semiconductor chips. Due to similar driving factors, the South Korean stock market followed suit in late April, surpassing the UK to become the world’s 8th biggest stock market (with Taiwan in 7th place). Not a good month for the UK…

This AI chip boom is also having a material physical impact on the electricity system in Taiwan. This is another clear similarity with Ireland, which I did not discuss in my original article. Both Taiwan and Ireland have a very large share of their electricity consumption being diverted towards electricity-intensive high-tech industry. In Taiwan’s case, semiconductor manufacturing, and in Ireland, data centres.

In Ireland about 22% of power was consumed by data centres in 2024, while in Taiwan about 23% of electricity was consumed by the semiconductor and electronics industry in the same year. TSMC alone accounts for about 8% of Taiwan’s electricity consumption, given its critical role in the global semiconductor supply chain. Similarly to Ireland, demand from semiconductor fabrication facilities is forecast to grow rapidly, with TSMC adding gigawatts of additional demand from new fabs in science parks in the south of the country, near the cities of Tainan and Kaohsiung.

Nuclear Restarts

Just two weeks before I arrived in Taiwan, President Lai Ching-te of the Democratic Progressive Party (DPP) announced that a restart plan for two nuclear power plants would be submitted to the Nuclear Safety Commission, reversing the DPP’s longstanding policy to abolish nuclear power.

As I discussed briefly in my previous article comparing Ireland and Taiwan, the DPP’s pledge to phase out nuclear power by 2025 under the so-called ‘nuclear-free homeland policy’ was achieved in May 2025 with the shutdown of Taiwan’s last active reactor (Maanshan Unit 2).

Energy policy, specifically nuclear, is actually a very politically important topic in Taiwan. In August 2025, three months after that final shutdown, a referendum asked whether Maanshan Unit 2 should be restarted. Nearly three-quarters of those who voted said yes, but turnout fell short of the legal threshold, so it failed. The government moved to restart the plants anyway.

Specifically, the Kuosheng Nuclear Power Plant and the Maanshan Nuclear Power Plant (located on the very southern tip of the island) were selected for the restart plans after Taipower’s preliminary evaluations found the plants fit for reactivation.

The Kuosheng plant is actually pretty close to Taipei, on the northern coast of the island. Being the energy nerd that I am, while visiting the Yehliu Geopark, which is located very nearby, I decided to get a closer look at the power plant myself. Taipower actually runs a funny little museum adjacent to the power station, which has a half-scale replica of the reactor core, among other energy explainer installations. I was able to get a pretty good view of the reactor buildings from a nearby pier, which was populated by many local Taiwanese fishermen, seemingly unperturbed by their proximity to a nuclear power plant.

The 1,970 MW power plant was commissioned in December 1981. According to the Taipei Times, personnel will likely begin to remove fuel rods from the reactor core by the end of this year, with the overall restart schedule running roughly a year behind Maanshan (possible restart as early as 2029).

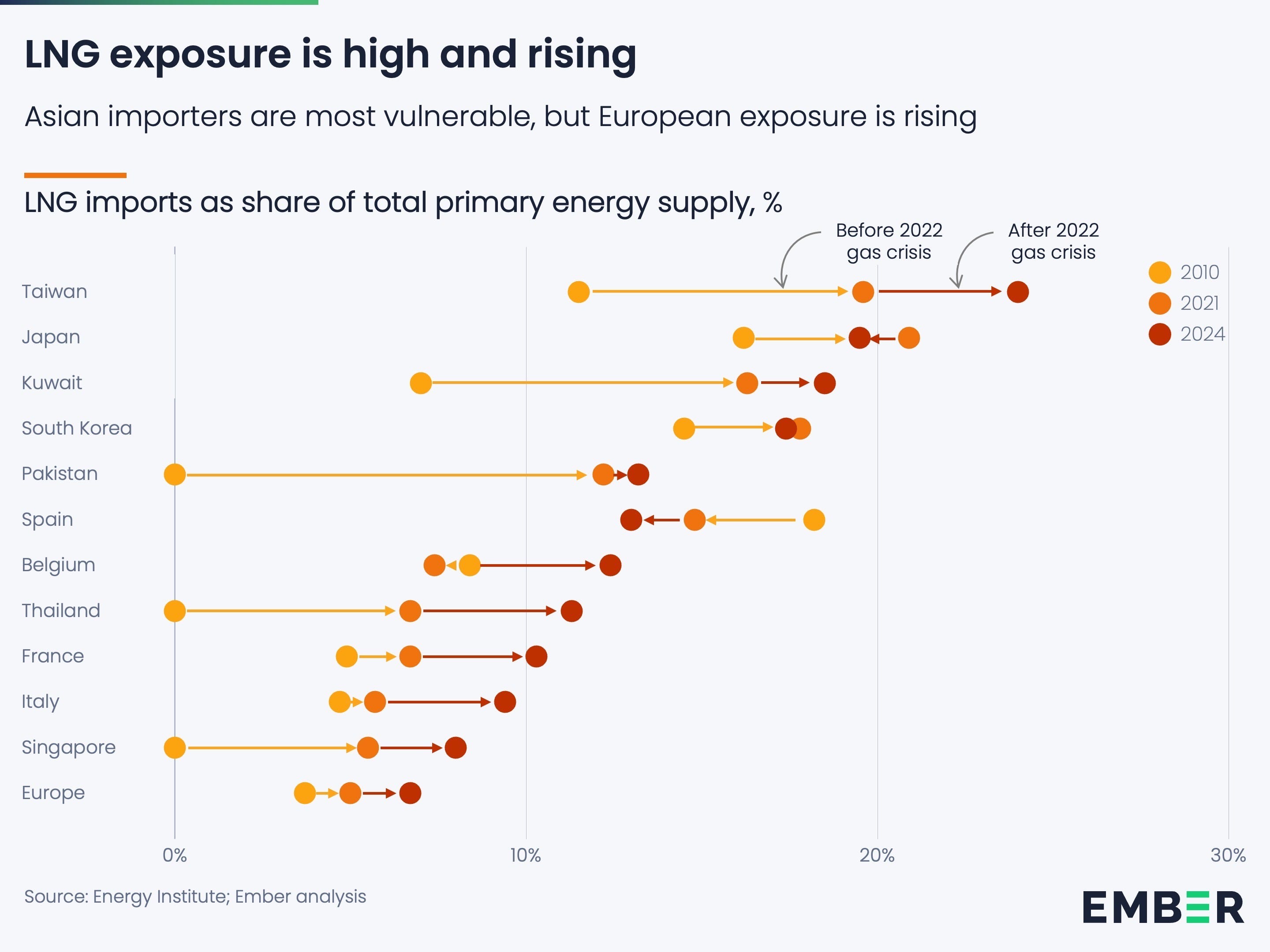

If these nuclear power plants can be restarted relatively easily and at a reasonable cost, it’s pretty difficult to argue against doing so. Taiwan is tremendously dependent on fossil fuel energy imports, which is a critical energy security vulnerability for the island.

Ember published an interesting analysis recently showing the LNG import exposure of various nations across the world and how this has changed since the 2022 energy crisis following the Russian invasion of Ukraine. Taiwan tops this chart, with LNG imports as a share of total primary energy supply exceeding 20% in 2024.

This energy security vulnerability, coupled with the phase-out of nuclear power generation, has also been a key motivator for Taiwan’s push into offshore wind (the topic that initially sparked my interest in Taiwan’s energy sector). Unfortunately, I didn’t get to witness any offshore wind turbines on my trip. However, I did get a glimpse of several small onshore wind turbines dotted along the western coastline when I was flying in to Taipei and on the 300km/h bullet train running down the coast to Taichung. These appeared to be small turbines, maybe 2 MW or so.

When I was flying out of the country, I got a clear view of the port of Taipei, and Century Wind Power’s manufacturing facility at the port. I could see about half a dozen huge jacket foundations sitting in the dockyard, ready to be transported offshore.

These likely belong to the Fengmiao 1 project being constructed by Copenhagen Infrastructure Partners. The jackets are close to 100 m tall and weigh over 2,700 tonnes. I discuss this project as a useful case study for the Irish offshore wind market (among other topics) in a webinar I was invited to give in late April after my trip. I covered the challenges and infrastructure requirements that it takes to build fixed-bottom offshore wind at water depths exceeding 60 metres. For those who missed the webinar you can view the recording here. I’ve also attached a copy of the slides below for those interested.

In an attempt to visually summarise some of the conclusions from my Ireland-Taiwan article, I’ve been playing around with the new Claude Fable 5 model while it’s still available on the Pro plan. The video below is a visualisation of some public GEBCO bathymetry data for the waters surrounding Taiwan.

The green shelf to the west (water shallower than 65 metres) represents areas where fixed-bottom turbines are viable. This area gives way to the amber band, buildable only with floating platforms (out to roughly 300 metres, the deepest yet deployed for floating), and then drops into the deep blue of the trench beyond, which falls to nearly 6,800 metres off the east coast.

Anyway, Taiwan is a great place to visit. I'd highly recommend it.

Interesting write up, but please note your chart incorrectly refers to Taiwan as part of China. This is inaccurate, please correct.